The auto market is changing again. This time, the pressure is coming from financing.

More people are taking longer loans and carrying higher balances. At the same time, vehicle values are less predictable than they used to be.

On the surface, nothing seems wrong. Payments are being made. Cars are still on the road.

But the risk is there. It just hasn’t shown up yet.

The Issue Most Drivers Overlook

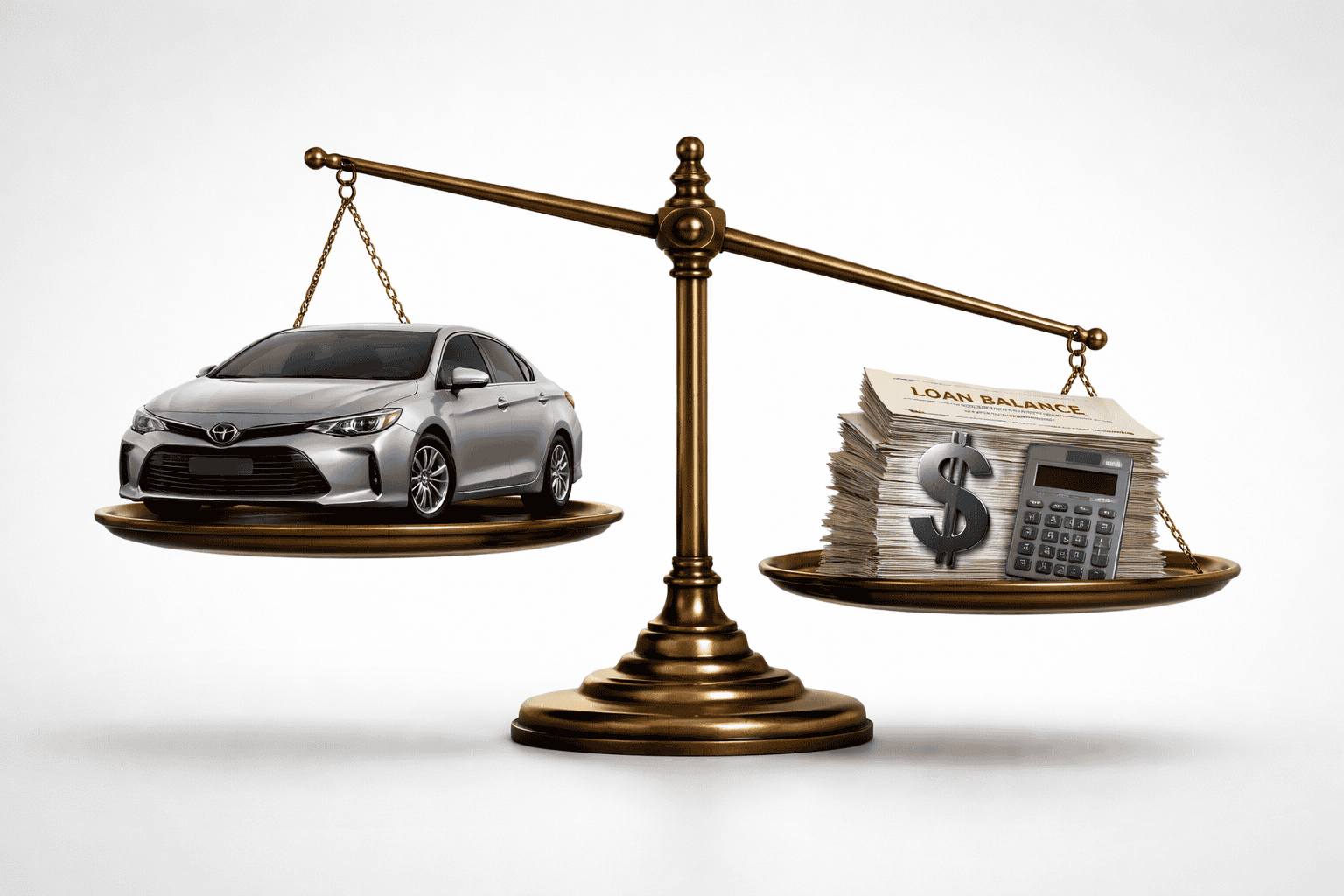

A growing number of drivers owe as much as their vehicle is worth, or more.

That doesn’t feel like a problem during normal ownership. As long as the payments are manageable, everything seems fine.

The issue only shows up when something forces a valuation.

An accident. A total loss. An insurance claim.

That’s when the numbers actually matter.

What Happens During a Claim

Insurance companies don’t look at your loan balance. They look at market value.

If you’re not familiar with how that process works, it’s worth understanding how claims, appraisals, and total loss valuations are handled in practice.

If your vehicle is worth less than what you owe, that difference doesn’t go away. You are responsible for it.

In a stable market, this gap might be small.

Right now, it isn’t always small.

Why This Is Becoming More Common

Several things are happening at the same time.

Loan terms are getting longer.

Interest rates have increased the total cost of financing.

Some buyers are rolling existing debt into new loans.

At the same time, vehicle values are not moving in a consistent way across the market.

This combination creates more exposure than most people realize.

The Problem With “Standard” Valuations

Most people assume the number they receive from an insurance company reflects true market value. In reality, initial offers can fall short, especially if you don’t know what to look for when reviewing a settlement offer. That isn’t always the case.

Valuations are based on internal systems, comparable vehicles, and general assumptions. Those methods can produce reasonable estimates, but they are not always precise.

Inconsistent pricing across regions and conditions makes this even harder.

Two similar vehicles can end up with different valuations depending on how the data is interpreted.

Where Money Gets Lost

In most cases, the loss happens at the moment a settlement is accepted.

Once that number is agreed to, the process is closed.

There is no adjustment later, even if the valuation was low.

Most drivers don’t challenge the number. Not because it’s accurate, but because they don’t have a clear alternative.

Why an Independent Appraisal Matters

An independent appraisal gives you a documented, data-backed value for your vehicle.

It allows you to compare the insurance offer against a more detailed analysis.

That alone can change the outcome of a claim.

In a market where small differences in valuation can mean thousands of dollars, having that reference point matters.

Final Thoughts

Auto lending risk is not just a lender issue.

It affects vehicle owners directly. It impacts how much equity you have, and how much you recover if something goes wrong.

Right now, those gaps are becoming more common.

Before You Accept Any Settlement

If you are dealing with an insurance claim, it is worth understanding your vehicle’s actual market value before accepting an offer.

A professional appraisal provides that clarity and helps avoid leaving money on the table.

Download This Article as a PDF

Prefer to read this later or share it?